Water damage insurance coverage protects your home and belongings from sudden, accidental water-related losses—such as burst pipes or appliance leaks—and filing a claim involves documenting the damage, notifying your insurer quickly, and supporting repairs with evidence and estimates.

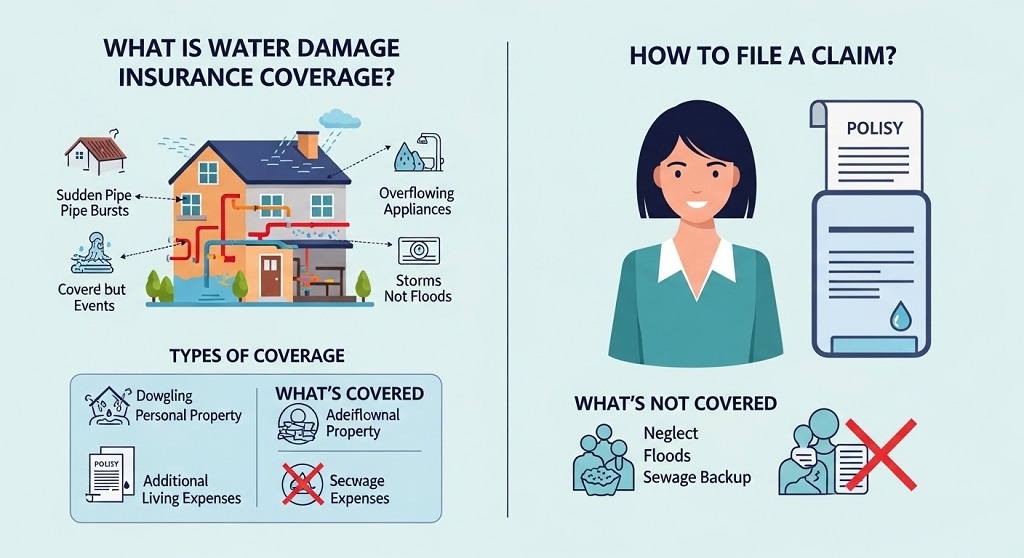

What Is Water Damage Insurance Coverage?

Water damage insurance coverage pays for repairs and replacement costs when unexpected water events damage your property, depending on the cause and your policy terms.

Water damage is one of the most common home insurance claims worldwide. Standard homeowners insurance typically covers sudden internal water incidents but excludes gradual leaks, neglect, and flooding from natural disasters unless additional coverage is purchased.

This type of protection applies to:

- Structural components like walls, ceilings, and flooring

- Electrical wiring and built-in fixtures

- Furniture and personal belongings

- Temporary accommodation if your home becomes unlivable

Without adequate coverage, repair costs from water-related incidents can escalate quickly. Even a minor pipe burst can damage drywall, insulation, wiring, and flooring within hours.

Why Is Water Damage One of the Most Common Insurance Claims?

Water damage claims are frequent because plumbing failures, appliance leaks, and weather-related issues happen regularly and often spread quickly before detection.

Insurance industry estimates suggest that a significant percentage of homeowners file at least one water damage claim during their lifetime. Unlike fire or theft, water incidents occur silently and escalate fast.

Common triggers include:

- Burst or frozen pipes

- Leaking washing machines or dishwashers

- Overflowing sinks or toilets

- Roof leaks during storms

- Blocked drainage systems

Even small unnoticed leaks can cause mold growth within 24–48 hours, increasing restoration costs significantly.

What Types of Water Damage Are Covered by Home Insurance?

Home insurance usually covers sudden and accidental water damage but excludes gradual deterioration and flooding from external sources.

Coverage depends on whether the event was unexpected and unavoidable. Policies generally protect against internal incidents rather than environmental flooding.

Covered Water Damage Events

- Burst pipes during cold weather

- Accidental appliance leaks

- Overflow from plumbing fixtures

- Roof leaks caused by storms

- Water damage from fire suppression systems

Events Typically Not Covered

- Floodwater entering from outside

- Groundwater seepage

- Long-term maintenance neglect

- Slow pipe corrosion

- Unrepaired roof deterioration

Understanding these distinctions helps prevent unexpected claim denials.

Does Homeowners Insurance Cover Flood Damage?

Standard homeowners insurance does not cover flood damage caused by rising water, rivers, storms, or heavy rainfall entering from outside.

Flood coverage typically requires a separate flood insurance policy. This applies to:

- River overflow

- Storm surge

- Flash floods

- Urban drainage failure

- Coastal water intrusion

Homeowners living in flood-prone areas often benefit from adding dedicated flood protection to avoid major financial losses.

What Does Water Damage Insurance Typically Pay For?

Water damage insurance usually pays for structural repairs, damaged belongings, cleanup services, and temporary relocation expenses if the home becomes unsafe.

Coverage often includes multiple components designed to restore both property and living conditions.

- Drywall replacement

- Flooring restoration

- Electrical system repair

- Furniture replacement

- Mold remediation (when linked to covered events)

- Professional water extraction services

Policies may also reimburse hotel stays or rental costs if repairs require temporary relocation.

What Factors Affect Water Damage Insurance Coverage Limits?

Coverage limits depend on policy type, deductible amount, property value, and optional endorsements added to the insurance plan.

Insurers calculate compensation based on:

- Replacement cost vs actual cash value coverage

- Policy deductible thresholds

- Maintenance history

- Cause of damage

- Documentation quality

Higher-value homes often require extended replacement cost endorsements to ensure full reimbursement.

How Do Replacement Cost and Actual Cash Value Differ?

Replacement cost coverage pays to repair or replace items at current prices, while actual cash value coverage subtracts depreciation from the payout.

| Feature | Replacement Cost | Actual Cash Value |

|---|---|---|

| Payout Amount | Full replacement price | Reduced by depreciation |

| Premium Cost | Higher | Lower |

| Financial Protection | Stronger | Moderate |

| Best For | Long-term homeowners | Budget-conscious policyholders |

Choosing replacement cost coverage significantly improves recovery after major water damage.

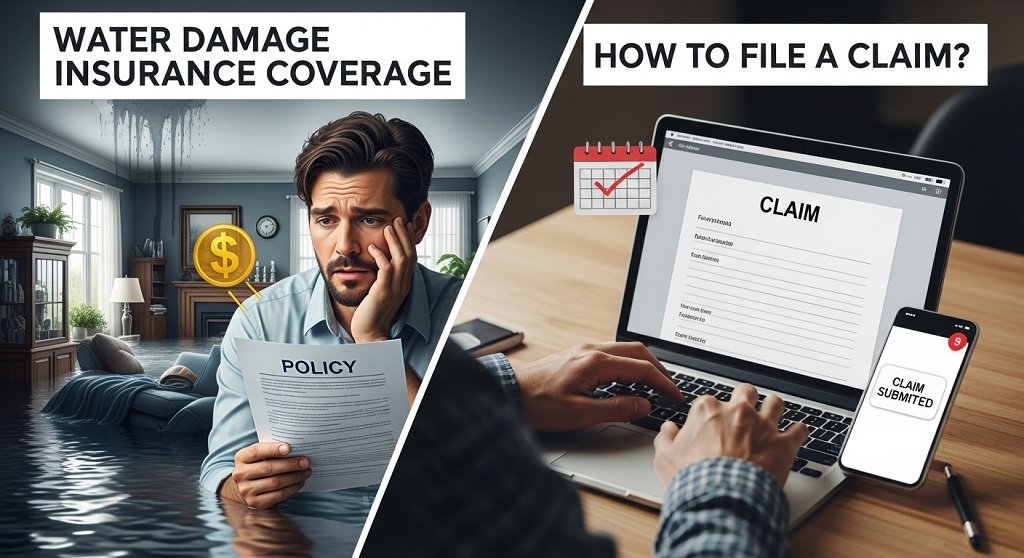

How Do You File a Water Damage Insurance Claim Step by Step?

To file a water damage claim, document the damage immediately, stop the source if possible, notify your insurer, and submit repair estimates with supporting evidence.

Step 1: Stop the Water Source

Turn off the main water supply or isolate the leaking appliance to prevent further damage.

Step 2: Document Everything

Take photos and videos showing affected areas before cleanup begins.

Step 3: Notify Your Insurance Company

Contact your insurer promptly through their claims hotline or digital portal.

Step 4: Prevent Additional Damage

Use temporary measures such as tarps or drying equipment if safe.

Step 5: Schedule an Inspection

An adjuster evaluates the extent of structural and property loss.

Step 6: Submit Repair Estimates

Provide contractor quotes and receipts to support reimbursement.

How Long Do You Have to File a Water Damage Claim?

Most insurers require claims to be reported within a few days of discovering the damage, though timelines vary by policy and region.

Delays may result in reduced payouts or denial if insurers believe the damage worsened due to inaction.

Prompt reporting strengthens claim credibility and accelerates settlement processing.

What Documents Are Required for a Water Damage Claim?

Typical claim documentation includes photos, repair invoices, maintenance records, and a written description of the incident.

- Date and cause of damage

- Photographic evidence

- Damaged item inventory

- Receipts or purchase history

- Professional inspection reports

Detailed documentation improves approval speed and payout accuracy.

Does Insurance Cover Mold Caused by Water Damage?

Insurance usually covers mold remediation only when it results directly from a covered water event like a burst pipe or sudden leak.

Mold from neglected maintenance or long-term humidity exposure is typically excluded.

Early drying within the first 24–48 hours significantly reduces mold risk and strengthens claim eligibility.

What Are the Most Common Reasons Water Damage Claims Get Denied?

Claims are often denied when insurers determine the damage resulted from neglect, gradual leaks, or uncovered flooding events.

- Delayed reporting

- Lack of maintenance records

- Pre-existing structural deterioration

- Policy exclusions

- Insufficient documentation

Reviewing your policy before filing helps avoid unexpected claim rejections.

Can You Prevent Water Damage Insurance Claim Disputes?

Yes, maintaining your home regularly and documenting repairs reduces disputes during claim investigations.

Preventive measures include:

- Annual plumbing inspections

- Roof maintenance checks

- Appliance hose replacement

- Gutter cleaning

- Leak detection sensor installation

These steps demonstrate responsible ownership and strengthen claim approval likelihood.

Should You Hire a Professional Restoration Company Before Filing a Claim?

Hiring a restoration professional early can prevent further damage and provide documentation that supports your insurance claim.

Certified restoration teams:

- Extract standing water quickly

- Prevent mold growth

- Dry structural materials

- Provide inspection reports

- Assist adjuster coordination

Many insurers recommend approved restoration partners to speed claim processing.

Conclusion: What Should Homeowners Do After Experiencing Water Damage?

Homeowners should act quickly after water damage by stopping the source, documenting losses, contacting their insurer, and preserving repair evidence to secure compensation efficiently.

Water damage insurance coverage plays a critical role in protecting property value and financial stability after unexpected plumbing failures, appliance leaks, or storm-related roof issues. Understanding what is covered—and what is excluded—helps homeowners respond confidently during emergencies.

Fast reporting, strong documentation, and preventive maintenance significantly improve claim approval outcomes. Reviewing your policy today ensures you are prepared before the next incident occurs.

If you have not checked your coverage recently, now is the right time to review limits, exclusions, and optional endorsements that strengthen long-term protection.

Frequently Asked Questions About Water Damage Insurance Coverage

Does homeowners insurance cover leaking pipes?

Yes, homeowners insurance typically covers sudden pipe leaks but excludes long-term unnoticed leaks caused by poor maintenance.

Is ceiling water damage covered by insurance?

Ceiling damage is usually covered if caused by a sudden internal leak or storm-related roof failure included in the policy.

How much does insurance pay for water damage repairs?

Insurance payouts depend on coverage limits, deductibles, and whether the policy uses replacement cost or actual cash value valuation.

Will filing a water damage claim increase premiums?

Yes, premiums may increase after claims, especially if multiple incidents occur within a short timeframe.

Can you claim water damage from a neighbor’s property?

Yes, if the neighbor’s negligence caused the damage, their liability insurance may cover repair costs.

Does renters insurance cover water damage?

Renters insurance usually covers personal belongings damaged by internal water incidents but not structural repairs to the building.

Is basement water damage covered by insurance?

Basement coverage depends on the cause—internal pipe leaks are often covered, while groundwater seepage usually requires additional protection.

Read More Also: How to Choose Plumbing Tools for Home Use

Discover More: How to Choose a Lightweight Vacuum for Hardwood Floors Easily